Whitechurch Investment Update: Quarterly Review - Q4 2022

11th January 2023

Click here to download a PDF Version of the Quarterly Review

Welcome to the Whitechurch quarterly investment review. This review covers the key factors that have influenced investment markets over the past quarter and the Whitechurch Investment Team’s current views and broad strategies being employed.

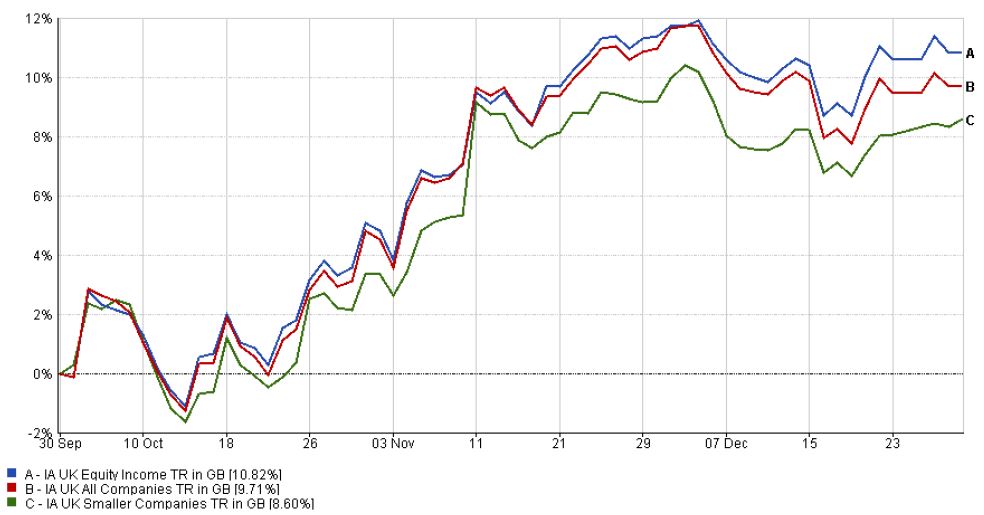

UK Equities

In stark contrast to Q3, the last three months of the year saw the wider UK market deliver an aggregate return of 9%. In what was another mixed quarter, share prices started the period by regaining some of the losses from a very disappointing September, with strong performance during October and November in particular. The rally did not continue throughout December however, with the UK market finishing the month at a net loss. Despite large cap stocks outperforming their mid and small cap counterparts year-to-date, it was the mid cap market which registered the biggest gain in Q4, returning 9.8%, versus 9.1% and 5.7% for large and small cap stocks respectively. Several factors contributed to the significant market recovery, with hopes from investors that inflation in the US has already passed its peak sat chief among them. By sector, there were widespread gains, with positive contribution from basic materials (+16.8%), healthcare (+12.4%), utilities (+12.4%), consumer discretionary (+11.8%), industrials (+10.3%), financials (+9.8%), energy (+5.9%), real estate (+4.5%), consumer staples (+3.6%) and technology (+3.1%). The only notable laggard was telecommunications (-9.6%). The UK was among the strongest of all the major regions during the period, second only to Europe.

Following on from a very challenging previous quarter, Q4 began with a relatively sharp recovery across global equity markets, with the UK in particular continuing to benefit from the preference among investors for so called ‘value’ stocks i.e., those in the more cyclical and lowly valued areas of the market perceived to be underappreciated. Broadly speaking, investors are still favouring companies which are profitable today, rather than those that may be profitable at some point in the future. As such, 2022 represents the most significant period of outperformance for ‘value’ over their ‘growth’ counterparts in more than 20 years. UK equities, as with global markets generally, reacted well to the continued downward trend in US inflation numbers, with markets appearing to largely ‘price in’ any policy changes from central banks during the quarter. In the case of the UK, there were no surprises from the Bank of England (BoE), who increased rates as anticipated, by 0.75% in November and 0.5% in December, taking them to the highest level in 14 years.

Despite UK inflation levels remaining extremely high, investors took some encouragement that the last CPI figure of the quarter (10.7%) came in 0.4% lower than November’s published figure. Despite no obvious trajectory, investors remained hopeful that UK figures will soon mimic those in the US, which have now experienced five consecutive months of contraction. Should inflation ease, the expectation is that central banks will no longer need to be aggressive with their interest rate policy, thus eventually creating a more normalised borrowing environment again. Other UK economic data released throughout the period was broadly encouraging too, with an improvement in retail sales, services output and consumer confidence figures. Sterling also gained 8% on the US dollar, finishing the quarter at the £1: $1.21 level. However, UK manufacturing output did decline to its lowest level since Q2 2020. I reported in November’s monthly commentary that the Office for Budget Responsibility now forecasts for real household income in the UK will be 7% lower in April 2024 than it was in April 2022, as well as a 1.5% contraction in GBP during 2023, compounding the gloomy outlook statements from both the BoE and International Monetary Fund.

Global Equities

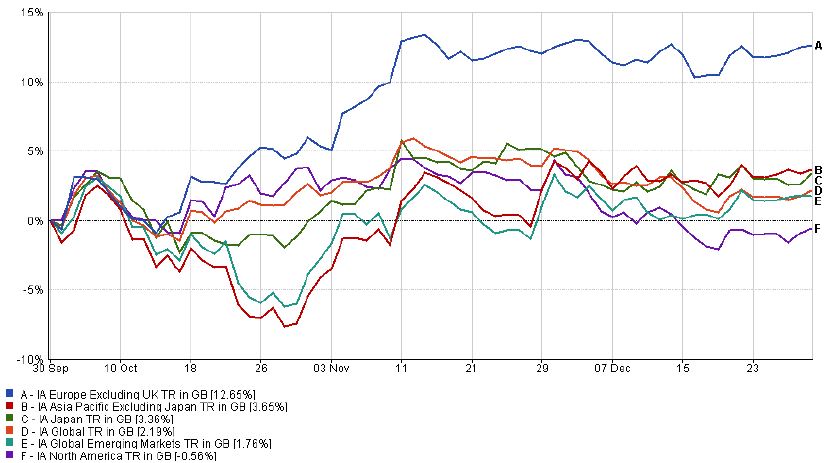

In contrast to last quarter, almost all major regions registered positive returns in Q4. Thanks to two strong months in October and November before a sharp decline in December, developed markets returned aggregate growth of 9.4%. The main driver for the former was the aforementioned notion that US inflation may have already peaked earlier in the year, which underpinned a broad recovery across major asset classes throughout much of the period. As I have been reporting in the recent monthly commentaries, there have also been several other factors at play, such as the relatively robust corporate earnings in the US, the much-needed stability in the UK political landscape and the switch in investor mindset away from the inflationary view that has dominated much of the year, to a more traditional recessionary one. I also reported that Chinese equities provided an additional driver of markets during November, following the government’s decision to ease certain strict Covid restrictions after more than two years. Global equities did, however, finish the quarter with a volatile month, particularly in the US, as investors began to weigh up the near-term recessionary outlook and what that might mean for the next corporate earnings season.

The US was the worst performing major region during Q4, largely thanks to a relatively sharp sell-off in December. After registering mid-single-digit growth in October, November and December were far more subdued, with all three major US equity markets suffering in the last few weeks of the quarter. Inflation figures in the US retracted, finishing the quarter at 7.1%, helped by factors such as the low dependence on overseas energy and the thus far stronger than expected economic data. There were no real surprises from the US Federal Reserve (Fed), with interest rate increases of 0.75% in November and 0.50% in December already anticipated. However, despite the general optimism for a ‘soft landing’ (that is for inflation and interest rates to normalise next year and for the US to avoid a deep or lingering recession) from investors, the cost of living is still high, and the Fed now expects to have to increase rates to higher levels and for a longer amount of time than previously thought. Although economic data has generally been stronger than expected, there are clear headwinds which also began to weigh on US markets towards the end of the quarter. There was a slowdown in the US property market, with transaction rates in both the new and second-hand markets in decline. Manufacturing and services output contracted too, with the former at its lowest point since early pandemic levels, as per the UK. Unemployment edged higher but the jobs market remains stronger than consensus forecasts from earlier in the year.

By contrast, European equities were the best performing of the major regions with the most influential French and German markets recording growth of 12.8% and 14.8% respectively. The majority of the gains were made early in the quarter, as markets reacted positively to the announcement of bloc-wide plans to tackle the ongoing energy crisis, in addition to the notable country-specific tailwind from the German government, who announced a €200 billion support package for households and businesses. As a result, producer prices in Germany declined for the first time in over 20 years. Despite there seemingly being no end in sight for the ongoing conflict in Ukraine, Q4 saw a notable improvement in the economic data that had been so poor year to date. There were surprises on the upside in both consumer confidence and manufacturing and services output throughout the quarter, with sentiment improving further on the release of December’s Eurozone inflation figure, which at 10.1% represented the first decline since June 2021. Sentiment was also supported by a significant reduction in the cost of European natural gas. The European Central Bank increased interest rates by 0.75% in late October and by 0.50% in December, in line with the Fed and BoE.

Japanese equities returned low-single-digit returns in what was a relatively eventful quarter. Given the cyclical nature of Japanese markets, they benefited from the broader equity rally, with gains made in both October and November. This was supported by a generally stronger than expected Japanese corporate earnings season. I reported in last month’s commentary how despite central policy focusing on supporting businesses and households in order to keep inflation below the 3% level, the most recent data release showed that inflation had reached 3.7% - the highest since the 1980s. The real surprise came in December, when the Bank of Japan (BoJ) announced that they are no longer averse to increasing the yields on long-dated government bonds by up to plus or minus 0.50% of the zero target, rather than the previous range of plus or minus 0.25%. The news was viewed as significant by global investors given the country’s reputation for being the only remaining developed economy with extremely loose monetary policy. Despite BoJ governor, Haruhiko Kuroda, denying the move represented a tightening of policy, the waning Yen strengthened by 4% shortly after the announcement, with Japanese stocks experiencing a sharp contraction.

Chinese equities experienced a volatile quarter, which started with a sharp sell-off in both Chinese and Hong Kong-listed markets in October as investors reacted badly to the announcement that Premier Xi Jinping would be in power for another five years, with the associated prospect of the prevailing ‘Zero Covid’ policy being extended. By stark contrast, November saw a significant market rally following a change of tack by the Chinese government. Following months of public unrest and pressure to ease some of the lockdown restrictions that had been in place for more than two years, policymakers announced the removal of some of the strictest rules with immediate effect. Despite an initial, and arguably anticipated, spike in cases as a result, December saw another significant announcement that China will be reopening its borders to international visitors in January 2023. Whilst a complete removal of restrictions seems unlikely in the near term, investors welcomed the policy changes as a step closer to a full reopening of the Chinese economy at some point next year. There were encouraging signs for an easing of geopolitical tension too, with both Xi Jinping and US President, Joe Biden, expressing that they would like to improve relations. Improved investor sentiment ultimately overshadowed the decline in both manufacturing and services output during the period, with the main Chinese and Hong Kong-listed markets finishing the quarter with gains of 2.1% and 18% respectively. There were also positive returns for other major Asian markets, such as Taiwan, Singapore and South Korea in particular.

Largely due to the significant inclusion of China, Emerging Markets as an asset class also experienced a volatile and mixed quarter. Following a very poor September, the period started in a similar vein before later recovering. Whilst there were positive contributions from Peru, South Africa, South Korea and Taiwan, there were losses for many other emerging countries, including India, Russia, Saudi Arabia and Brazil. It was an eventful period for the latter, where losses were led by a 12% decline in the share price of state-backed oil and gas giant, Petrobras, following fears that new President-elect, Luiz Inácio Lula da Silva, will be less supportive of the existing corporate model, and markets more generally, than his predecessor. Despite being the beneficiary of an apparent shift in manufacturing contracts, Indian equities failed to back up their year-to-date performance, with a disappointing quarter return, whilst Russia and Saudi Arabian markets were stunted by a reduction in energy costs. Emerging Markets still finished the period with an aggregate positive return, after the gains made in November and December, mainly driven by the aforementioned policy change from the Chinese government, saw all of October’s losses recouped.

Fixed Interest

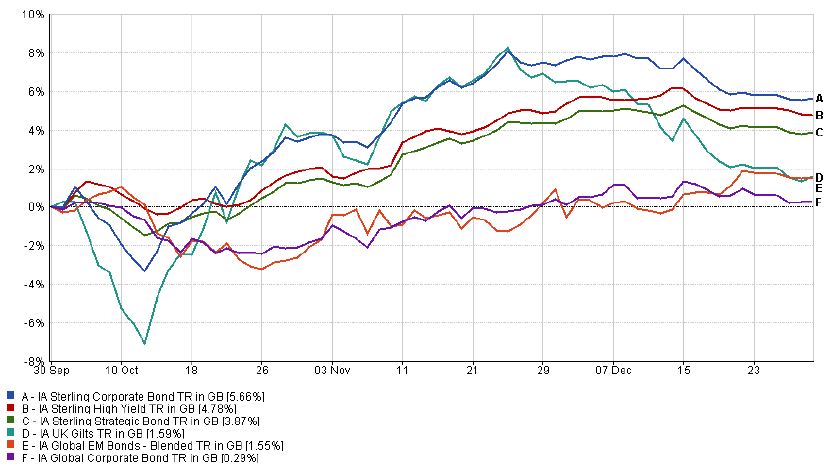

Global bonds returned an average of -1% during October, with mixed performance across regions and the credit quality spectrum. Given the sobering returns of -7% for the asset class during Q3, October’s numbers were generally well-received by investors. In the US, both Government and Investment Grade (that is those with a higher quality credit rating) suffered from interest rate rises (given the inverse relationship of yields and prices), with their lower quality High Yield counterparts outperforming. The yield of the 10-year US Treasury (often seen as a yardstick for medium to long-term investor sentiment and growth prospects) rose from 3.83% to 4.05%, with the shorter-dated 2-year counterpart remaining uncharacteristically higher, at 4.49%. UK Gilts were the standout performer during October, albeit from a low base, following the instatement of a new Prime Minister and Chancellor. The previously announced bond buyback programme from the BoE also broadly achieved its objective of stabilising the Index-Linked market following September’s debacle. It was a far less eventful month for other major bond markets, such as in Europe and Japan, with both remaining broadly flat throughout the month.

November saw somewhat of a recovery, with global bonds returning an average of 4.7%, with the relative rally playing out widely across the asset class. In the US, both Treasuries and corporate bonds registered low single-digit gains, following the seemingly already priced-in interest rate rise from the Fed. The yield of the 10-year US Treasury declined from 4.05% to 3.61% (meaning prices rose), with the shorter-dated 2-year counterpart remaining higher but declining to 4.34%. UK Gilts were again among the standout performers during the month, particularly the Index-Linked market. There were also positive returns for sterling investors from other major regions, such as Europe, Japan and emerging markets. Broadly speaking, it was those longer-dated bonds with higher duration (that is, a higher sensitivity to changes in interest rates) that outperformed, as, among other factors, investors viewed the US inflation pattern as a sign that the Fed will no longer need to hike aggressively for too much longer.

Despite December proving to be a relatively flat month for performance of much of the asset class, UK Gilts experienced a reversal in fortunes, declining 4.9% in the last month of the quarter. This was driven by the BoE unwinding its emergency purchasing programme by selling over £17 billion of long-dated and index-linked positions. This represented the sale of nearly 90% of the bonds they had bought in a two-week period shortly after September’s mini budget. This wrapped up a truly disappointing, and unprecedented in recent times, calendar year, with UK Gilts registering an aggregate loss of 24% in 2022. As I have been reporting periodically, last year’s pain was not limited to the UK bond market. I wrote earlier in 2022 that the collective losses of global bonds as an asset class in the first half of the year were the worst in more than a century. I also highlighted the significant lack of traditional diversification between the return profiles between bonds and their equity counterparts, which despite improving in the latter months, will almost certainly be remembered as one of the themes of the year in the minds of investors.

Commercial Property

The UK commercial property market doubled down on its poor Q3 with another single-digit loss in the most recent period, in what was only the second negative quarterly return in two years. As we reported last time, sentiment towards the sector is being damaged by the prospect of higher borrowing costs and the impact reduced household disposable income is expected to have on retail demand. The notable difference this quarter, however, was that listed property securities, as well as many Real Estate Investment Trusts (REITs), significantly outperformed their direct bricks and mortar counterparts. This was not surprising, given their inherent correlation with the wider listed equity market, and offered some respite following a difficult Q3. Macroeconomic indicators also continued to look weaker for the asset class, with the release of the latest UK Commercial Property Survey from the RICS highlighting that 81% of respondents now consider the market to be in a downturn. A decline in both primary and secondary market rents and capital values are now expected in the near-term, despite sentiment towards some areas remaining stronger than others – namely industrial and prime office space sectors. That said, occupier demand across office, retail and industrial all appear to be in decline, despite the latter remaining in positive territory for the time-being. We have highlighted in both monthly and previous quarterly commentaries that UK interest rate forecasts continue to pressurise the residential housing market too. However, there was some solace in Q4, with the latest consensus figures showing a slight reduction in expectations of how high the BoE will raise rates.

Commodities

With the exception of natural gas, it was generally a less volatile period for commodities compared to Q3, with the aggregate composite index for the asset class edging fractionally higher. The returns were mixed, with gains for both aggregate precious and industrial metals indices. The spot price of platinum and silver were the standout performers, both returning 17% respectively in sterling terms. Most of the price uplift came in December, aided by the prospect of a spike in demand from China given the government’s plans to ease lockdown restrictions. Industrial metals, such as steel and iron ore, also benefited, with the aggregate industrial metals index returning mid-single digit growth during the period too. Despite being an eventful year for oil, the price of Brent crude remained relatively flat during Q4, finishing the year at the $85 per barrel level. This does represent, however, a significant decline during the second half of the year, with the growing concerns over global economic growth in 2023 weighing on demand expectations. A big talking point of the quarter was the reduction in the price of natural gas, which declined by 42% in sterling terms, taking the price to a level last seen before the Russian invasion of Ukraine in Q1. The contraction was mainly driven by a very mild European autumn suppressing household demand for gas, with storage levels consequently remaining much higher than initially feared. Broadly speaking, prices finished the year approximately 60% below their 2022 peak, however, investors remain cautious that a cold snap in Q1 2023 could send prices significantly higher again.

Cash

Given the economic backdrop and the resultant upward move in fixed income yields, the case for holding cash remained popular with some investors during the quarter. In the short-term, cash deposits insulate investors from the price volatility seen in other asset markets. However, in the long-term, the real value of cash deposits is likely to continue to be eroded by inflation. We currently only hold cash for short-term tactical reasons or within lower risk strategies, where the risk profile dictates a need for a larger cash allocation.

Whitechurch Investment Team

Quarterly Review, Q4 2022

(Issued January 2023)

FP3492.06.12.2022

Click here to download a PDF Version of the Quarterly Review

Source: Financial Express Analytics. Performance figures are calculated from 01/04/2022 to 30/06/2022 net of fees in sterling. Unit Trust prices are calculated on a bid-to-bid basis OEICs, Investment Trust and Share prices are calculated on a mid to mid basis, with net income reinvested. The value of investments and any income will fluctuate and investors may not get back the full amount invested. Currency exchange rates may affect the value of investments.

Important Notes: This publication is approved by Whitechurch Securities Limited which is authorised and regulated by the Financial Conduct Authority. All contents of this publication are correct at the date of printing. We have made great efforts to ensure the accuracy of the information provided and do not accept responsibility for errors or omissions. This publication is intended to provide helpful information of a general nature and is not a specific recommendation to invest. The contents may not be suitable for everyone. We recommend you take professional advice before entering into any obligations or transactions. Past performance is not necessarily a guide to future performance. Investment returns cannot be guaranteed and you may not get back the full amount you invested. The stockmarket should not be considered as a suitable place for short-term investments. Levels and bases of, and reliefs from, taxation are subject to change and values depend on the circumstances of the investor.

Copyright 2025 Whitechurch Financial Consultants | Website designed by The Smarter Web Company