Quarterly Review - Q3 2024

9th October 2024

Click here to download a PDF Version of the Quarterly Review

Welcome to the Whitechurch quarterly investment review. This review covers the key factors that have influenced investment markets over the past quarter and the Whitechurch Investment Team’s current views and broad strategies being employed.

Macro

After a relatively benign first half of 2024, Q3 saw a sharp increase in volatility and a change in market leadership, as US large caps gave up ground to other, less heavily owned parts of the global stock market, including the UK and China. Despite the sharp drawdown in early August, all markets outside of the US finished the quarter in positive territory, reminding investors that in times of volatility, often the best course of action is to take no action at all.

July began in a relatively subdued fashion, with little to hint at the volatility to come. Having fallen sharply through 2023, US inflation had proved ‘sticky’ through early 2024. After a decline of around 6% from its peak, it looked as though the final leg of the inflation journey – from 3% back down to the US Federal Reserve’s 2% target – would prove the hardest. June’s data (published in July), which showed a tick down in headline inflation to its lowest reading in three years, was therefore broadly welcomed. Arguably the biggest story of the month was political, as incumbent US President Joe Biden officially ended his campaign for a second term, yielding to party donors after a disastrous presidential debate. Elsewhere, the UK market enjoyed a rare moment in the sun, as favourable macroeconomic data hinted at a more promising outlook for an equity market dogged by persistent outflows in recent years.

In early August, July’s US jobs report put an abrupt end to the low volatility backdrop. A surprise uptick in unemployment, coupled with a sharp slowdown in the number of new jobs added, saw recession fears spike, with many investors questioning the strategy of the Federal Reserve – had it waited too long to cut rates? Fears of a US recession rippled through global equity markets, with developed regions all sharply down. For Japanese investors, worse was to come, as perceived weakness in the US economy, coupled with a surprise interest rate hike by the Bank of Japan, triggered a mass unwind of the yen ‘carry trade’. The subsequent rapid strengthening of the yen led to a sell-off in Japanese equities which saw large caps fall nearly 20% – their largest three-day drop in recorded history. However, as the month progressed and recession concerns eased, markets largely recovered, serving as a timely reminder of the benefits of having a long-term investment horizon.

September saw the return of some normality, at least for developed markets. After much speculation, the Federal Reserve announced its first 50-basis point interest rate cut, following in the footsteps of the European Central Bank (ECB) and Bank of England (BoE), which cut rates (albeit by 25 basis points, rather than 50) in June and August, respectively. Most analysts expect the Federal Reserve to announce further cuts before the end of 2024, although uncertainty remains about the magnitude and timing.

Perhaps the most notable headline through September came from China, where the People’s Bank of China (PBOC) announced a new combination of stimulus measures designed to boost the struggling domestic economy. The PBOC had announced similar, smaller scale measures earlier in the year. However, the scale of the latest round appeared to catch the market’s eye; Chinese large cap equities rallied over 20% in the second half of the month. While the positive price momentum is welcome news for those with a Chinese equity allocation, only time will tell if the latest stimulus package has the desired effect on the Chinese economy.

Markets

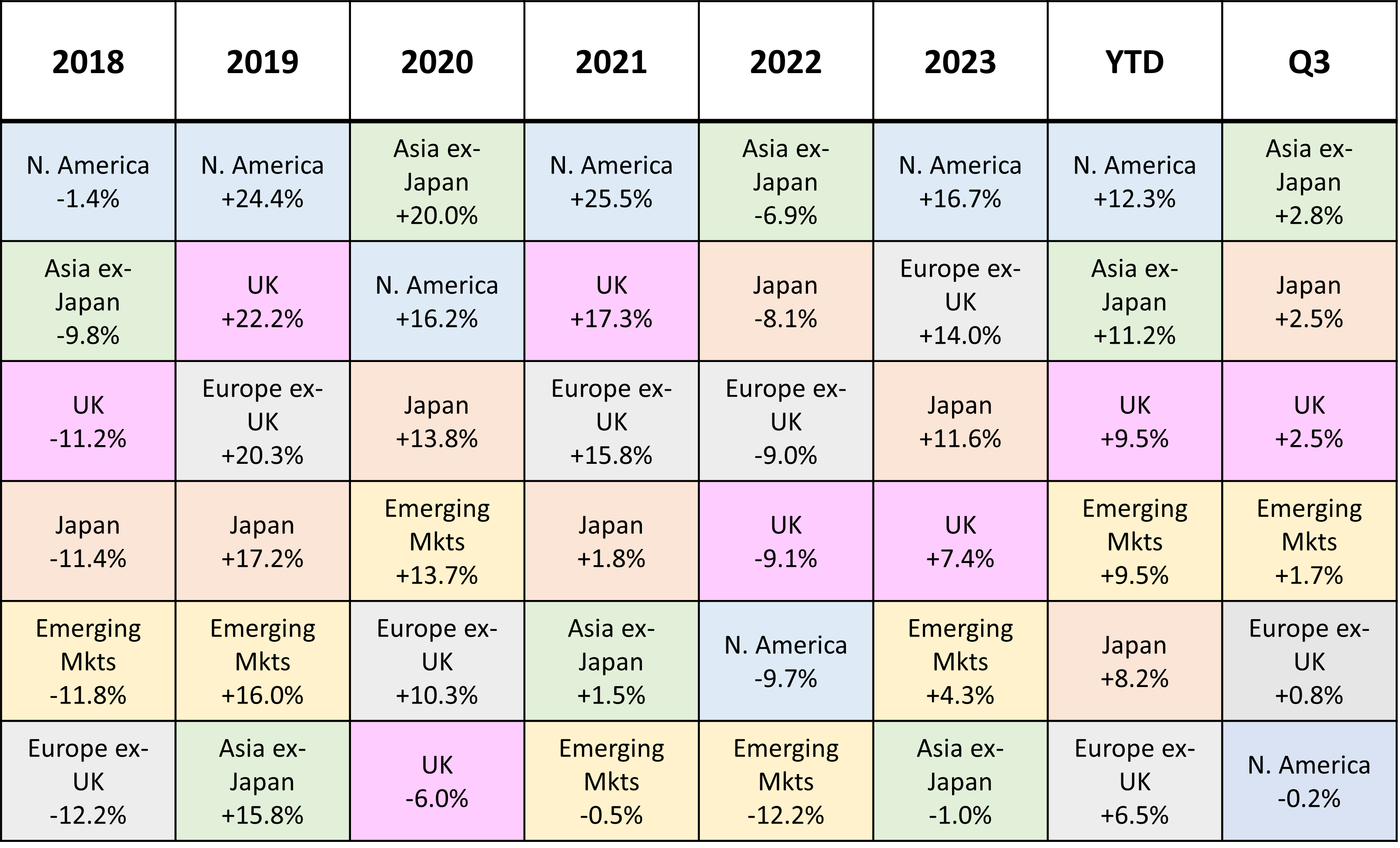

Moving on to markets, where all regions outside of the US produced positive absolute returns. While US equities recovered fairly quickly from early-August lows, they still slipped to a muted loss over the quarter (-0.2%), as investors mulled the likely path of interest rates and what that might mean for the health of the world’s largest economy. In a reversal of recent fortunes, several of the mega-cap technology names struggled, with Nvidia down over 7% despite another strong set of earnings. Microsoft followed suit as investors questioned the stretched valuations of some of the world’s largest companies.

Japan (+2.5%) was the best performing developed region through Q3, despite the record-setting drawdown in August. The rapid appreciation of the yen relative to other major currencies was a tailwind for unhedged overseas investors, while the news from neighbouring China also appeared to have a positive impact towards the end of September. The UK (+2.5%) produced a similarly positive return, with at-target inflation and a persistent discount relative to other developed markets offsetting concerns about the upcoming autumn budget. The Eurozone was more muted (+0.8%) – despite a second 25 basis point rate cut in September, markets remain concerned about the growth outlook. German manufacturing remained a notable weak spot, as it continued to struggle in the face of higher energy costs and weak demand from China, a key region for exports.

In sharp contrast to previous quarters, it was China that provided the strongest returns, as the announced stimulus measures saw aggregate equities recover from a nearly 10% loss in early September, to a greater than 10% gain by quarter close. The outperformance of Chinese equities also drove gains for Asia ex Japan and global emerging market indices, with the former the best performing major region through Q3. Elsewhere in emerging markets, there were gains for India (+1.1%) and Brazil (+1.0%), while more technology heavy indices such as Taiwan and South Korea tracked the US lower.

Major market total returns in Sterling. Data correct as of 01/10/24. Sectors used: Asia ex-Japan – IA Asia Pacific excluding Japan TR (GBP), Emerging Mkts – IA Global Emerging Markets TR (GBP), Europe ex-UK – IA Europe excluding UK TR (GBP), Japan – IA Japan TR (GBP), N. America – IA North America TR (GBP), UK – IA UK All Companies TR (GBP).

Global bond markets were mixed, but it proved a better quarter for sterling investors. With bonds now paying a real yield (i.e., a yield greater than the underlying rate of inflation), investors can benefit from the income component of fixed interest assets while waiting for a potential capital gain as and when rates come down. Bonds have traditionally served as an insurance policy against an economic slowdown, and in that regard the asset class demonstrated its worth in early August. While US recession fears prompted a sharp sell-off across global equity markets, bonds (particularly government issuance with minimal credit risk) rallied sharply. Longer-duration assets typically outperformed during this period, as markets ramped up bets on interest rate cuts by the Federal Reserve. However, as the quarter progressed and recession fears eased, it was more economically sensitive sectors which generally outperformed, with high yield (+3.5%) once again the top performer. In contrast, gilts (+1.8%) lagged on a relative basis.

Some of the strongest returns came from alternative sectors, particularly more rate sensitive asset classes such as listed property (+8.8%) and infrastructure (+6.9%). Both sectors have faced significant headwinds in recent years, but their outperformance against the backdrop of a weakening US economy reaffirmed the diversification benefits they provide. Also of note was the strong performance of UK-listed renewable energy assets, including The Renewables Infrastructure Group (TRIG, +11.3%). The sector was a major beneficiary of both the growing anticipation of future rate cuts, as well as what many investors perceived to be a more supportive political backdrop following Labour’s win in July’s General Election.

Asset Allocation & Portfolio Activity

Note that the following discussion is not an exhaustive list of changes made and due to the individual model mandates, changes discussed may not apply to every Whitechurch portfolio – for full details on activity within a specific strategy, investors should revert to the fact sheet.

Following a relatively busy second quarter, activity was minimal – we feel the portfolios are well positioned to benefit as the rate cutting cycle begins in earnest across developed markets, while significant exposure to more defensive areas of the market, including global equity income and infrastructure, should provide a degree of protection if the US economy begins to slow meaningfully.

Fixed Income

While we made no changes to the portfolios’ fixed income allocation over the quarter, the majority of our chosen underlying managers have been increasing the duration (interest rate risk) of their respective funds in recent months, as they position for the rate cutting cycle. At portfolio level, we remain slightly underweight duration relative to major indices, largely as a result of our allocation to short-dated investment grade corporate bonds. While the backdrop for duration has improved in recent months, we remain happy to pick-up yield in short-dated issuance, while benefitting from the lower overall volatility profile of the asset class. With markets now arguably pricing in an overly optimistic number of rate cuts for the coming months and year, shorter duration assets also provide a degree of downside protection, particularly in the event of any unexpected upticks in inflation.

Quarterly Outlook

The inflation narrative has not changed materially in recent months – headline data continues to recede, and in the case of the Eurozone, is now below the ECB’s 2% target – but core inflation remains sticky and is likely to remain a headache for central bank policymakers through the remainder of 2024. In the US, economic momentum remains, and recession risk (which would likely force the Federal Reserve into a greater number of cuts) remains low. While the Federal Reserve, ECB and BoE are all expected to continue cutting rates, to us the market looks to be pricing in an overly optimistic number of cuts. This presents a risk for those overly exposed to duration and in our view justifies an ongoing allocation to short-dated bonds.

As inflation has normalised, the relationship between equities and bonds has returned to more traditional footing, which should bode well for multi asset portfolios. The outlook for equities is mixed depending on region, but broadly positive on aggregate. We still feel the US looks expensive relative to other developed markets, but we are more constructive on areas of the market that have fallen out of favour in recent years, including the UK, Europe, and small caps. It remains to be seen whether China’s most recent round of stimulus measures will prove the turning point for the region, but with most stocks still trading at near rock-bottom valuations, this could prove an attractive entry point for long-term investors. A weaker dollar (which we anticipate as US rates fall) should act as a tailwind for emerging market economies more generally; we continue to allocate to Chinese equities and the broader emerging market sector across the higher risk portfolios.

The bond market may be being overly exuberant in its pricing of interest rate cuts, but the yields on offer remain attractive despite the recent rally. Whether or not the market is accurately forecasting the trajectory of future cuts (it did a very poor job of predicting rates as they went up), we are now firmly in the downward portion of the rate cycle. Appetite for bonds is likely to remain as investors look to lock in the high yields on offer, and with the US and UK economies on firm footing, at least in the short term, corporate bonds still look attractive.

While we have seen the first leg in the recovery for many of the rate sensitive sectors that suffered as rates rose, there appears to be significant further upside for alternative asset classes such as property and infrastructure. We like the latter in particular, as it combines a degree of rate sensitivity with defensive qualities, while providing diversification versus global equities.

| Whitechurch Securities Ltd Investment Team | October 2024 |

Whitechurch Investment Team

Quarterly Review, Q3 2024

(Issued October2024)

FP3820.09.10.24

Important Notes: This publication is issued and approved by Whitechurch Securities Limited, a division of Whitechurch Securities Limited which is authorised and regulated by the Financial Conduct Authority (FCA). We have made great efforts to ensure all content is correct and do not accept any responsibility for errors or omissions. All information is intended to be of a general nature, will not be suitable for everyone and should not be treated as a specific recommendation. We recommend taking professional advice before entering into any obligations or transactions. Investment returns cannot be guaranteed, past performance is not a guide to future performance and investors may not get back the full amount invested. Stockmarkets are not a suitable place for short term investments. Levels, bases of, and reliefs from taxation are subject to change and values depend on circumstances of the investor.

Our Environmental, Social, and Governance (ESG) Credentials:

Whitechurch Securities Limited are fully committed to the FCA’s AntiGreenwashing Rules and have a robust process to ensure all our ethical investment strategies are managed to strict mandates. However, as we rely on third party fund managers for the underlying investment decisions, we cannot guarantee that our own ESG criteria are being met 100% of the time, despite our best efforts to do so. Our ESG fund screening, selection, review and ongoing monitoring process is available on our website or upon request.Data Protection: Whitechurch may have received your personal data from a third party. If you invest through us, we may use your information together with other information for administration and to make money laundering checks. We may disclose your information to our service providers and agents for these purposes. We may keep your information for a reasonable period in order to manage your investment portfolios. We record telephone calls, to make sure we follow your instructions correctly and to improve our service to you through training of our staff. You have a right to ask for a copy of the information we hold about you and to correct any inaccuracies. When you give us information about another person you confirm that they have appointed you to act for them; that they consent to the processing of their personal data, including sensitive personal data and to the transfer of their information and to receive on their behalf any data protection notice.

Whitechurch Securities Limited is authorised and regulated by the Financial Conduct Authority. Financial Services Register No. 114318.

Registered in England and Wales 1576951. Registered Address: C/o Saffery Champness, St Catherine’s Court, Berkeley Place, Bristol, BS8 1BQ

Correspondence Address: The Old Chapel, 14 Fairview Drive, Redland, Bristol BS6 6PH Tel: 0117 452 1208 Web: www.whitechurch.co.uk

Copyright 2025 Whitechurch Financial Consultants | Website designed by The Smarter Web Company